.png)

While the core four areas—team, product, traction, and market—are consistent evaluation criteria across company types, the ways investors evaluate them differ depending on the type of company.

Consumer Social companies (described in Part 1 above) are unique for a couple of reasons, such as the tendency for them to be high risk but high reward, and that they delay monetization until the network-effect is well established. In other sectors, like Consumer Subscription, market size and monetization are often a part of the discussion even as early as the seed stage. Because the consumer is often the one paying for the service, gauging their willingness to buy the product is often a key criteria for evaluating early product market fit.

The goal of this guide is to demystify the fundraising process and help founders better understand the nuances of how investors evaluate consumer subscription companies. At the same time, it’s worth keeping in mind that the criteria in this guide are far from fixed and vary between firms and investors.

Green means you should feel confident to pitch. Yellow is maybe, there’s some potential, but it’s not a slam dunk. Red is going to be a non-starter for most professional VCs.

Download the full evaluation rubric here.

Vision:

Regardless of sector, the founder’s vision is typically a key component of any investor’s evaluation. In addition to accurately describing the current state of the business, founders must be able to paint a picture of the long-term vision for the company.

We often call talking through the long-term vision “dreaming the dream” because this is usually the best case scenario for the company. The long-term vision is not the five-year financial plan, but the transformation shift that occurs if the business is successful in achieving its goals.

As a reminder, the economics of venture capital are such that even the most successful funds hinge on just a handful of big wins. In order to underwrite an investment, an investor needs to believe that your company has the potential to be one of these big wins—even if it is far off in the future. Oftentimes, founders at the early stage are too focused on short-term execution (i.e. how to get to their first $1M in revenue) that they forget to walk the investor through how the opportunity could eventually return their fund.

Truly special founders give you the sense that they were, for one reason or another, “compelled” to pursue this idea. This can come in many shapes and sizes, but the story must be authentic. Founding startups is hard, so it’s important that founders are motivated by more than just the potential financial upside.

Unique Insight:

No matter how brilliant the idea, every early-stage founder must be able to answer the question, “Why you?” It is important for a founder to be able to clearly articulate the unique perspective, experience, and skillset they bring to the table. In the best case scenario, a founder has had unique exposure—either personally or professionally—to the pain point they are trying to solve and has realized something that only appears to others with the same vantage point. The insight doesn’t have to be huge, but it needs to be unique enough that it will provide an acute advantage over potential competitors.

Melanie Perkins, co-founder of Canva, got her start teaching design students programs like InDesign and Photoshop. She saw first hand just how challenging these legacy programs were to use. She started her first design software business, Fusion Books, targeting the design and creation of school yearbooks. The unique insight she gained through that experience led her to launching Canva with the audacious goal of democratizing design.

Team Gaps:

Just as founder vision is a critical component of any venture, investors look for the completeness of the founding team. In many ways, a team is only as strong as its weakest link. A product visionary will struggle without a technical co-founder to execute their ideas. Similarly, the best coder in the world will build a mediocre product if the product vision is unclear. This dynamic can make fundraising tricky for solo founders. While not impossible, it is challenging for one individual to wear so many hats. That means many institutional investors prefer to invest in founding teams rather than solo founders.

Magnitude of Pain:

It’s always a big hurdle for companies to convince users to try an unproven solution, especially in the early days. No matter how good your product is, consumers like buying products that they’ve heard of before. In order to get a consumer to try something totally out of the blue, their pain point must be so acute and pressing that they are desperate for a better solution. As Unusual’s co-founders Jyoti Bansal and John Vrionis preach in our Academy, only desperate customers buy from startups.

Sean Ellis created a nifty test for measuring early signs of product market fit. He suggested that companies could gauge their fit by simply asking their users “How would you feel if you could no longer use the product?” After benchmarking nearly a hundred startups, Ellis found that companies with the best growth metrics almost always had more than 40% of their users answer “very disappointed.” (i.e. 58% of Superhuman users and 51% of Slack users) While this metric constantly fluctuates, it is a core indicator that you are solving a real problem for your users.

Immediate Value:

Consumers are fickle. If they don’t receive immediate value from your product, it is unlikely that they will continue to pay for it. There are a few exceptions to this rule—like aspirational products (gym memberships) where consumers buy something they want to use, not one that they actually use—but these consumer bases often face attrition over time.

A great example of a product with an immediate “aha” moment is Zoom. The product allows users to be ushered into a high quality video meeting with only one-click. It’s simple to get started and the value is apparent right away.

Repeatable Behavior:

Investors like subscription products because revenue is more predictable. Because of this, many companies have tried to create a subscription product in order to win over investors, even when the model doesn’t make sense for their users. In my mind, there are two key reasons that make a product a good fit for subscription:

1) The product is consumable: In this case, we don’t mean consumable like a food—but rather, the product gets “used-up” and thus requires frequent replacement. A classic example of this is Dollar Shave Club. DSC did not invent the razor. However, the fact that razors get dull over time and consumers consistently have to buy new razors made the market ripe for subscription. In addition to physical goods, content—like TV/movies (Netflix, Hulu), workouts (Classpass, Peloton), meditation (Headspace, Calm)—is also consumable. In contrast, big one-time purchases like mattresses (Casper) or suitcases (Away) don’t make sense as subscriptions.

2) Value accrues over time: The more you use the product, the more valuable it becomes. This dynamic is true for anything habit-forming (i.e. meditation apps). These products usually store valuable information (i.e. productivity tools) and require some upfront work to get set up. This creates behavior that makes consumers come back consistently—a precondition for a good subscription product. Spotify is a great example where the value accrues over time. Not only are your playlists saved onto your account, but the recommendation engine gets to know you and your preference with usage. Even if another music streaming service were to become available, many consumers would be hard pressed to switch and start from square one with a new service.

Acquisition:

We generally recommend that startups begin with a narrow target user who has the most burning need for the solution that the startup provides. Having a narrow target user is one of the most critical steps to honing a product, finding traction, and proving distribution. The graphic below shows the broadening of the user base over time. Each subsequent ring of customers is further and further from the initial target user.

Unless network effects are at play, customers’ characteristics get worse as you broaden away from the initial target user. With each adjacent ring, the magnitude of pain the customer experiences diminishes and the customer will become more expensive to acquire.

You often see this with paid user acquisition. Reliance on paid advertising may allow for a quick bump in growth initially, but will likely cause challenges down the road as the cost increases. It will also likely mean that the company will be heavily reliant on venture funding and will require many subsequent financing rounds to fuel growth. This means most investors have a strong preference for growth driven by organic acquisition, which is a more sustainable option for growth over time.

The “Sent via Superhuman” sign off is a brilliant example of a product feature that helped fuel organic acquisition. For each email a user sent using the product, the user shared the service with whomever they were sending the email. This feature helped Superhuman to reach new potential customers organically.

Retention:

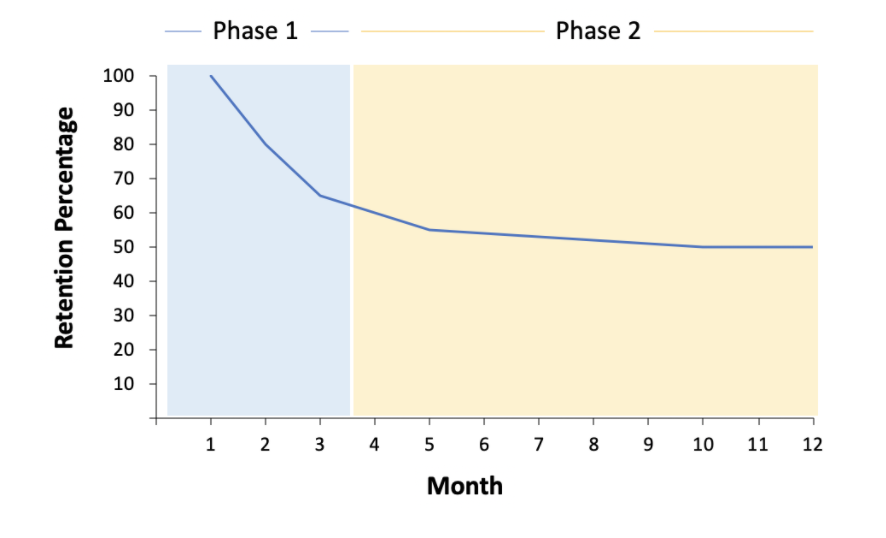

Once customers are acquired, it is important to understand how likely they are to stick around. Especially for subscription products, retention has a direct correlation with lifetime value (LTV) of the customer. Retention can be divided into two main phases shown in the graph below:

Phase 1: This shows the initial drop off over months 1, 2, and 3. It’s perfectly normal to see a drop off here. Users that churn in these early months never really get into the repetitive cycle of using the product. They may have had trouble getting started or the product might not be what they were expecting. As teams collect data on why these users are churning, it’s important to address these issues.

Phase 2: This represents the steady-state churn of “actual” users. In the best-case scenario, the graph will begin to flatten out relatively quickly. This flatness demonstrates that for engaged users, the product is very “sticky”. This stickiness is indicative of a strong LTV and a healthy business.

Meditation apps are examples of businesses likely to have a steep drop off after month one. Meditation is an aspirational concept, and many users never even get started. However, once users develop a habit of meditation, the product becomes very sticky. Companies like Calm have designed clever product features like the “Daily Calm” to encourage users to keep coming back to the app every day.

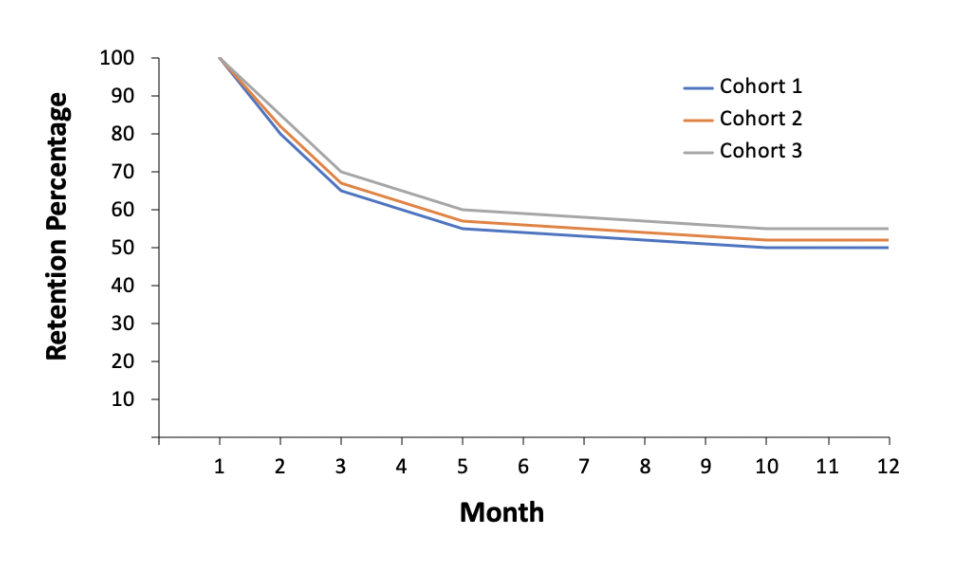

Cohorts:

Just as acquisition costs increase as you broaden the aperture of target customers, retention characteristics may also change. Cohort analysis is the best way to identify and analyze this change. In the base case scenario, cohort analysis shows that customer behavior is improving over time, indicating network effects at play or the product improving at scale.

Here is an example of what a strong cohort analysis might look like using the above retention curve:

For more information on cohort analysis, check out our Unusual Primer on Cohort Analysis.

Market Size:

This is a somewhat obvious one. The bigger the market, the less of it you have to capture to become a massive company. Fintech is a great example of a massive market. Because Fintech is a vital service to nearly everyone on the planet, the market is big enough to support multiple billion dollar companies. That said, there are other factors that can make a market compelling beyond just size. A market that is small, but growing rapidly can also be a great opportunity since there may be more room for new entrants. Productivity Tools is an example of a recent market that grew very quickly. A company like Notion has seen impressive growth, but may not have seemed like a big opportunity when the company was first getting started.

Market Characteristics:

Some markets are big, but the dynamics are not conducive to building a large/valuable business. In order to make a case for why there is an opportunity in a given market, there should be some clear technology advantage such as network effects or economies of scale. This can come in many forms, but a founder should be able to articulate why a big company should exist in the space and, more importantly, why now is the time to build it.

A few key questions that we like to ask about the market:

Example: A shift from brick and mortar to e-commerce paved the way for subscription offerings like Amazon Prime and StitchFix.

Example: A shift to remote work created huge growth opportunities for companies like Zoom and Slack.

Example: A shift to on-demand content allowed companies like Netflix and Hulu to quickly surpass legacy players like Blockbuster, Redbox, and Tivo.

Value Expansion:

Opportunities for upselling can be great mechanisms for value creation. As companies get bigger, it is easier to upsell existing customers rather than acquire new ones. Showing ways that you can become more valuable to your user over time is a very promising premise for growth. For example, a women’s competitor to Dollar Shave Club called Billie started off by selling razors, but quickly expanded into other adjacent products like lotion and shampoo. The company now sells a full suite of bath-related products via bundled subscriptions.

At the end of the day, “subscription” is simply a business model—not a product.

At Unusual we gravitate towards consumer subscription products that solve a clear pain point and exploit already repetitive behaviors. We prefer companies that, even at the early stages, show the core metrics of a scalable acquisition model with strong retention. Just because your business does not tick all the boxes, doesn’t mean that it’s not worth pursuing. While there is some conventional wisdom to what investors look for, each will evaluate the opportunity with a fresh perspective.