A loose rule of thumb for when a tech company can seriously consider an IPO is when they cross $100M in annual recurring revenue (ARR). While this ARR milestone is clear, what’s not always apparent to founders starting out is that the go-to-market you choose in the early stages will drastically alter how they get there and what their team will look like along the way.

In this post, we’ll outline the three most common go-to-market (GTM) motions, introduce their components, and show how they will impact the path to $100M ARR.

The three most common GTM motions for B2B enterprise companies today, in order of prevalence, are:

Each of these motions have their own strategy across these categories:

We will define each motion, provide examples of companies that execute it, and compare the differences in the aforementioned categories.

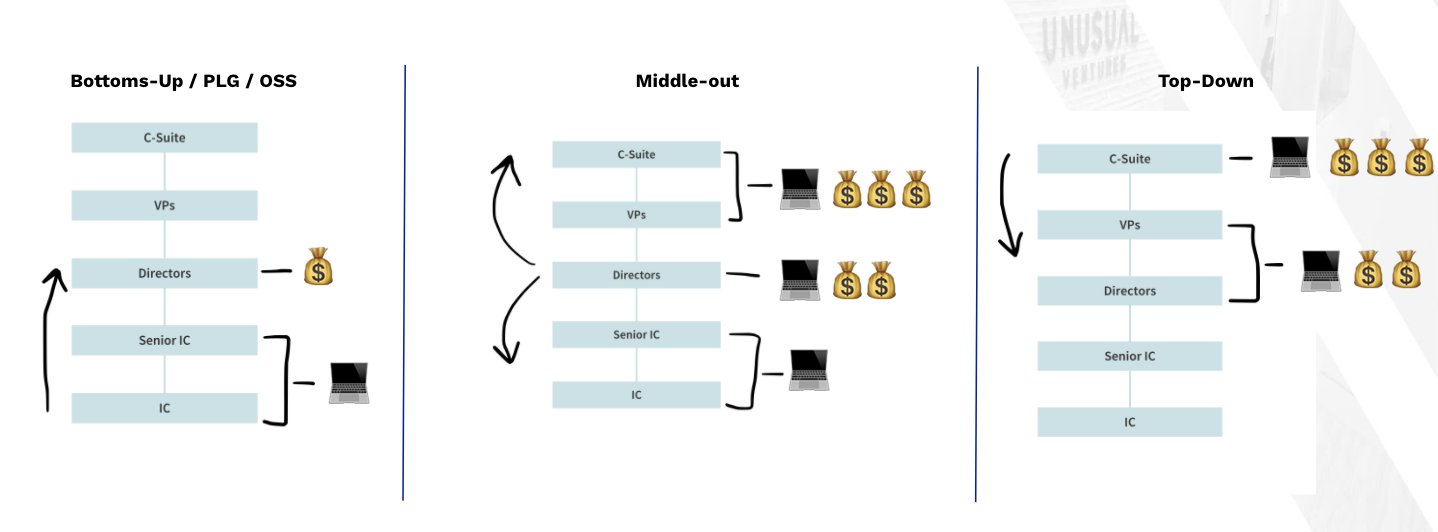

Easily the fastest-growing GTM model in recent years, bottom-up is defined by a self-serve, freemium, or open-source product where end users (typically individual contributors) will try, adopt, and potentially start paying for your product without any direct involvement from a sales team.

This motion is also synonymous with product-led growth (PLG), which has become the darling of product GTM given the success of companies like Datadog, Twilio, and Slack. In this motion, the product (through onboarding, OSS) does the selling, providing end users with easy installation and rapid time to value. Features that managers or other senior team members would value are usually kept behind a paywall.

Once you hit an inflection point for adoption, a sales team is then layered on top of PLG to start converting free users to paid, to bundle usage inside companies into one larger contract, or to go after net new business to command a higher average contract value (ACV).

For the sales process section, we will look at this through the lens of how prospects discover, try, and buy products and the internal teams in charge of those functions.

Discover (product marketing), Try (product/engineering), Buy (self-serve/sales)

Average contract values for the bottom-up motion tend to be the lowest of the three, usually coming in at or below $20,000.

Since trying and adopting products through PLG is so easy, companies can afford to have lower ACVs since they typically have rapid adoption and customer counts in the hundreds of thousands.

When it comes to team construction for this motion, since the product is your main “sales rep,” the first hires made by the founding engineering team are product and marketing.

When you need to hit the customer adoption milestones of a bottom-up strategy, your product experience has to be airtight. Since trying to have a sales rep or small sales team reach tens of thousands of prospective customers does not scale, product marketing hires become crucial.

Once you have the beginnings of an adoption flywheel, with hundreds or thousands of freemium, self-serve, or OSS users then you can bring on a sales rep or sales team to start converting them to paying customers or higher ACVs.

The middle-out GTM motion is the “have your cake and eat it too” of the three, taking advantage of PLG’s explosive growth with top-down’s higher ACVs.

Companies that execute this GTM motion have products that resonate with ICs, their direct managers, and VPs since the products here are usually deeper in the stack or span multiple teams (databases, data-warehouses, data-analytics, SIEM, etc.).

Since these products handle mission-critical data that impacts the day-to-day business and are tightly tied to revenue, they command higher ACVs. Decisions around these products aren’t made lightly or often (every three to four years), so they also execute a land-and-expand motion, starting with one application or workload then moving on to others inside a business until they have an opportunity to standardize.

When it comes to discovering middle-out products, product marketing will run campaigns along with sales reps prospecting into individuals or accounts that might have some engagement or are completely cold.

To try the product, there may be a freemium or OSS version, but for prospects to access features behind a paywall (support, advanced security, automatic management, etc.), a sales rep will take them through a product testing process.

Buying these products can also start off with freemium or self-serve amounts lower than $20K, but beyond that will be sales-driven with MSA’s and order forms.

Discover (marketing/sales), Try (product/sales), Buy (self-serve/sales)

The average contract value for these products falls between $24,000–$120,000 a year. These contracts can either be up-front, annual commitments, or annual commitments with monthly payment terms.

Since the products in this space deal with a lot of change management inside a prospects organization, around people, process, and new products — all while commanding a higher price point — sales teams need to be hired earlier in the company’s life cycle than bottom-up.

After the founding engineering team brings on a product team (if needed), a sales leader should follow since they will be a key part of the discovery, product testing, and purchasing process. They can also go out and evangelize for the product as well, but will need a marketing hire soon after to scale those efforts.

Then, once they’ve closed five to 10 accounts, a customer success or account manager will need to come on board to grow those relationships.

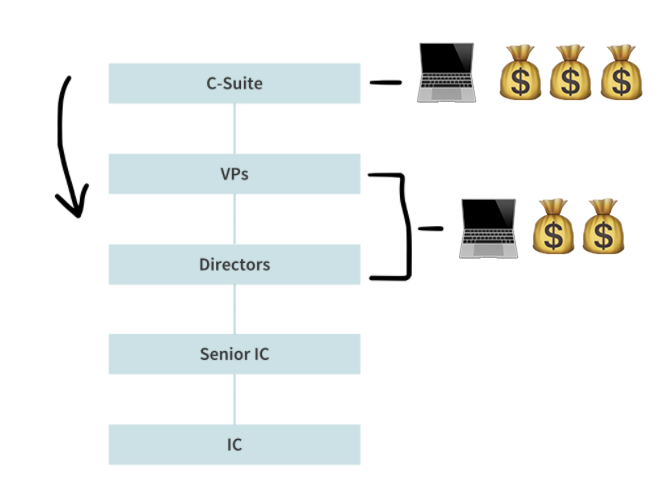

The top-down selling motion is the oldest out of the three and the least prevalent in recent years. This motion is based on a sales leader or sales team having relationships with the VP/SVP/C-Suite that picks a product for their team to use.

Products that use the GTM have the highest average contract value, but therefore also take the longest to close which is exacerbated due to the potential lack of adoption from ICs.

This was the default GTM 10–20 years ago when products were primarily introduced only by sales teams, but Bottom-Up/PLG has turned this on its head.

The sales process here is dominated by sales leaders and sales teams. Marketing will help with product discovery, but any product testing and purchasing will go through sales.

Discover (Marketing/Sales), Try (Sales), Buy (Sales)

One of the benefits of top-down selling is you start off with and have direct access to the individuals in accounts who control the budget. As a result, Top-Down has the highest ACV, between $120,000–$1,200,000.

While you’ll need less customers at this price point to hit $100M ARR, it will also take much longer per contract (100 days+) to close.

After the founding engineering team has a beta or GA, sales people are brought on to start getting in front of CEOs, CTOs, CISOs, CROs, etc. to be design partners or paying customers. This is usually followed by a marketing hire to pair with them.

Just because a company starts by pursuing prospects in one GTM motion doesn’t mean it can never change. Many of the companies above moved upmarket over time as their adoption grew. The same can be said for moving downmarket, but it’s important to call out that moving upmarket is almost always easier and more successful than moving downmarket. This is due to the implications each motion has for the product experience, product discovery process, pricing, and team composition as they grow.

Companies that aim to move upmarket tend to make product decisions early on that influence the ease of adoption, installation, growth, and retention of customers. This means there needs to be an easy way to sign up, use, and purchase the product. Converting users to paying customers or taking IC usage and bundling it into one larger contract is a motion that’s become standard for companies moving up market.

For those trying to move downmarket, the challenge becomes taking an expensive product that’s not easy to install or test without multiple people being involved in a multi-week POC and making it self-serve. It’s also harder to build out a business model that starts to prioritize more self-serve users at a significantly lower price point ($24K ARR compared to $150K) when it comes to forecasting. In general, more companies have found success taking a product whose adoption has been fueled by PLG and layering a sales team on top, rather than a product which was reliant on salespeople to sell it adopting PLG for the first time.

For the last section in this piece, let’s look at how those three GTM motions would impact a company’s path to hit $100M ARR.

First, let’s consider the five most prevalent paths to achieving the $100M ARR mark using the following prospect categories according to their ACV: Self-Serve, Small Business, Mid-Market, Enterprise, Large Enterprise.

Average ARR per category (with ranges)

That means the breakdown of how many customers you would need to reach $100M ARR for each path would look something like this:

To make this more concrete, here are examples of the companies above and the categories of prospects they started going after in their first few years. Two caveats: I’ve grouped some of them together since the lines between each are never as neat in the real world and all of these companies eventually went up or down market as they grew.

When you look at the companies that have crossed the $100M ARR mark (including those listed above), the majority of their revenue comes from Mid-Market/Enterprise customers with contracts between $20,000–$150,000, as shown in their ACVs from recent S-1s and earnings calls:

Companies that take a middle-out approach like those above have the second highest average AVC and have taken seven to eight years on average from formation to IPO.

Companies that have a bottom-up/PLG motion are crossing the $100M ARR mark faster than ever.

Years to cross $100M ARR

When it comes to ACV, they have the lowest of the three. For example, 54% of Asana’s customers pay >$5,000/year. If you average out total paying customers by ARR, that’s $158/customer, but their total ARR is still $190M due to volume of customers.

Zoom is another great example of PLG + Self-Serve/Small Business ACVs. They’re on pace to have over $2B in ARR this year, but at the time of their IPO last year, their ACV was just $6,000/customer.

While PLG can be a powerful way to drive more efficient conversions to paid usage, it’s not a GTM panacea by itself. Companies that successfully sustain their growth rates layer in sales teams on top of PLG.

In closing, founders should spend more time thinking about the GTM motion they intend to execute early on in their company’s journey since it will have an outsized impact on how prospects discover, try, and buy – and will determine what your team will look like as you continue to scale.

Continue on to Math of Sales.