Crypto trading, real-time business and peer-to-peer payments, personalized insurance, mobile digital wallets, vertically focused neo-banks — fintech’s rapid pace of innovation over the last five years has made these once-unthinkable ideas commonplace.

At Unusual Ventures, we are committed to fintech innovation with investments in high-growth businesses such as Carta and Robinhood, among others. With our recently announced ~$500M Fund III earlier this year, we are looking to build on these investments in the fintech sector.

For both financial institutions and non-financial companies, the opportunities to embrace software solutions to improve productivity and enhance consumer experience are at an all-time high. Even with the recent headwinds in the macro market putting pressure on certain segments of fintech like direct-to-consumer (DTC) lending and insurance, or Buy Now Pay Later (BNPL) companies, we believe over the long run, the fintech ecosystem is among the most powerful sectors to invest in.

In this post, we’ll provide an overview of the fintech landscape, share some of the investment areas we’re excited about, and offer some advice for founders that are building fintech companies.

Here’s an inside look at how we analyze core fintech segments including better access, data and workflow automation, and business enablers.

We segment fintech businesses into three categories, depending on the end customer:

This category includes better ways for consumers to bank, borrow, spend, and protect their assets. Some of the areas that have seen innovation include more financial access (often driven by better data on consumer risk) and the portability of account information across a consumers’ financial life.

While the traditional area of consumer applications have seen many players enter across different fintech industry verticals, new product lines continue to emerge. This includes banking products that target teenagers and young adults (HENRYs, aka High Earner Not Rich Yet) such as Greenlight and Current, and alternative asset investment platforms like Alto.

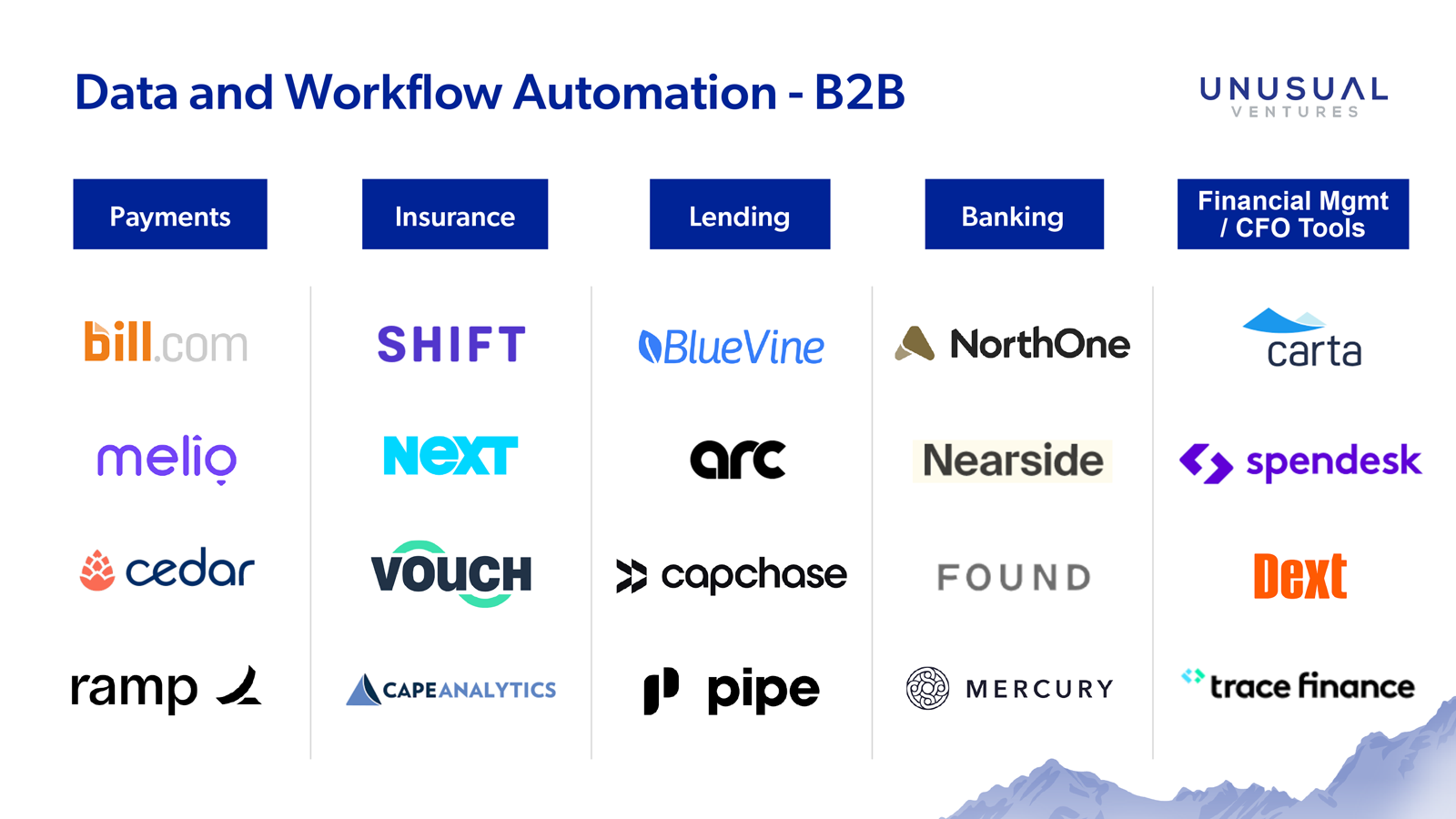

We typically define data and workflow automation tools as platforms that help financial and nonfinancial service institutions better transact, protect, and share their data with other business entities or improve their internal operations. This includes increased automation of internal financial services practices to streamline many of their operations and reduce manual headcount. B2B also includes more data analysis and underwriting to better assess risk when partnering with other financial entities and/or consumers. More recently, startups that provide upfront capital without dilution to SaaS startups have gained significant investor interest including Pipe and Arc along with startups that provide financial management platforms and tools for CFOs such as Carta and Dext.

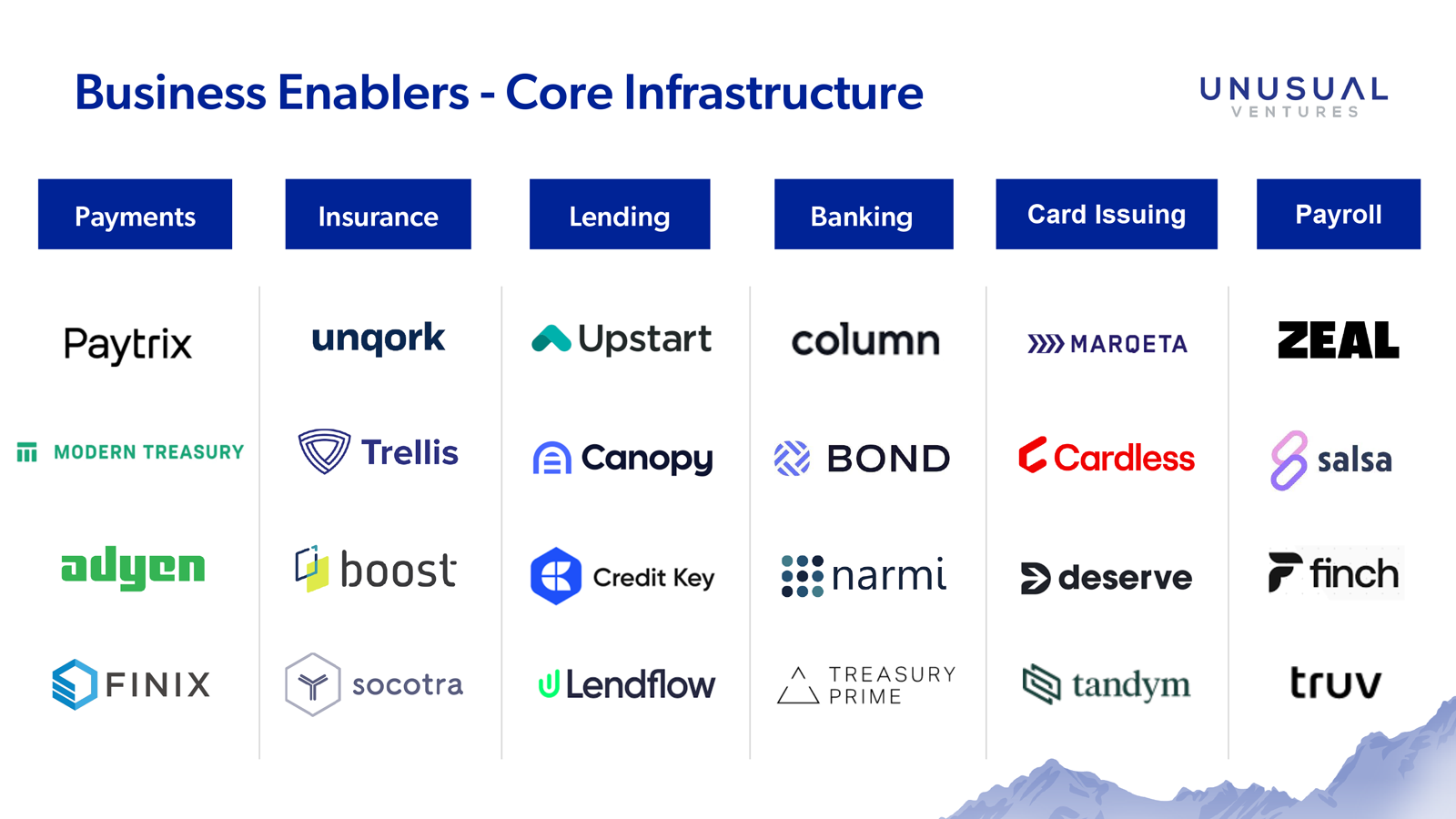

Core infrastructure includes cloud-native platforms that power the decision-making and management of users on these fintech applications. Infrastructure offerings have also evolved to include custom label solutions where startups that don’t want to go through the necessary regulatory approvals to become an issuing bank, but still want to offer financial products. These “as-a-Service” solutions including credit-as-a-service and banking-as-a-service allow startups to build financial products much more quickly and embed them into their finance flow. Many financial solutions are embedded on a company’s platform and can also build greater customer loyalty and increase LTV/spend. A great example is Starbucks and their massively successful loyalty application, which creates a closed-loop payments ecosystem.

One of the by-products of the global pandemic has been the rapid acceleration of digital banking, payments, and investing, which led to increased investment in fintech by VCs, including record amounts of funding in 2021. As more money has flowed into the sector, more companies are going after the same customer base, leading to rising customer acquisition costs. While these increased costs and challenging macroeconomic conditions have made some areas of fintech less attractive for investment, there are other areas of fintech that remain appealing over the long term, or have even become more enticing.

Tools for managing cash flow become a higher priority area as businesses look to navigate uncertainty and set themselves up for success in the subsequent macro-environment. Additionally, there will be increased pressure on managing expenses and headcount effectively, spurring more adoption of software automation for core financial functions within businesses. In a new economic environment, fintech will deliver value in these core areas creating better outcomes for consumers and businesses.

Many business practices across financial services don’t put data into practice regardless of the amount they capture and analyze. Acquiring the right data at the right time — and then keeping that data flexible, portable, and secure — are key challenges.

By leveraging data in real time, financial services companies can better understand their customers, provide them with enhanced experiences, and make improved decisions overall. This extends beyond just underwriting — businesses can determine what products to put in front of customers, present payment options that optimize profitability and automate core requirements like compliance management.

This is why we’re excited about orchestration layers for data in fintech. Many decision-makers are not technical and are unable to streamline their operations or make the most data-informed decisions. This includes incumbents with data sitting across different silos, startups that rely on APIs to pull data from various sources to create a summarized analytics, and crypto where it’s still difficult to bridge between TradFi and DeFi. Orchestration layers will allow nontechnical users to leverage and visualize data that may sit across multiple sources to make optimal business decisions.

Vertical software products that solve specific pain points and accumulate core insights into a customer’s operating data can be a natural on-ramp to offering embedded financial solutions. With this unique insight, SaaS companies are able to embed financial products such as payment solutions, underwriting, or insurance protection as part of their solution, providing an additional source of revenue.

Vertical SaaS players with embedded financial solutions have both a compelling product advantage and an attractive core software-based business model enhanced with fintech offerings. High growth businesses like Toast in the food/beverage space and AppFolio in the property management space are good examples in this category.

Giving users and enterprises digital access to their financial products and automating many of their functions has created immense value across the fintech value chain. This includes the rise of mobile-first neobanks like Chime and Revolut. While getting access to our financial assets has certainly gotten easier, new platforms continue to emerge, aiming to provide more business and customer segments with the financial products they need.

In the enterprise space, while digital access has largely penetrated much of the market today, automation still remains a challenge for many back-office functions of financial institutions. This is why we’re excited about enterprise-focused platforms that provide automation for back-office operations including tools for the CFO’s office. Given the number of manual processes and pain points that exist with incumbents today, we remain excited about the opportunity to back great founders in this category.

When you think of the largest fintech companies to date — Stripe, Plaid, Rapyd, etc. — what do they share in common? They all leverage APIs to transfer data between sources or integrate their own products into other interfaces. The API allows companies to more quickly offer and launch different financial products at a fraction of the cost and with short setup times.

These APIs have given rise to “as-a-Service” business models, where fintechs no longer have to acquire the necessary banking or regulatory licenses and can quickly offer and launch their own financial products. We believe these “as-a-Service” models will continue to evolve and develop new products for areas of the market that are still underserved.

At Unusual, when speaking with fintech founders, and looking at investments more broadly, here are some key questions we ask as we evaluate startups to build transformational businesses.

1. Is there a market inflection point?

While market size is obviously an important factor in evaluating a startup, we also focus on looking for a shift, change, or new development in a sector that creates the compelling “why now” moment.

It’s important to remember that market and timing need to come together, along with an exceptional team, to create a successful business with the right early momentum. We often see strong teams with interesting ideas, but when there is no critical insight into the question of What makes this a burning problem that my target customer set needs to solve now!?, we recommend founders recalibrate.

2. What is the leap?

We look for businesses attacking segments where there are still opportunities to make big leaps within software and infrastructure. If a business idea is just moderately better than current alternatives, more often than not, the status quo will win. Business inertia — not just other well-funded startups — is a real competitor.

Early stage companies that can clearly identify the one area where they are demonstrably better than existing alternatives have the best chances of early customer adoption and utilization. Similarly related, when we talk to design partners, we look for early evidence of the new solution helping make that “business leap” and for signs that there is an ongoing business need that will drive sustained usage and, ultimately, customer LTV.

3. Can this startup win in crowded segments?

Fintech has experienced a rush of venture investment that’s created crowded markets with lots of market noise. While you don’t need to be first in the market, you must believe you can become one of the top players in a market to truly build a large business of real value.

When there are dozens of well-funded companies in a space, it doesn’t mean you can’t compete, but you must ask yourself “what makes your specific product/solution a must have now for your Ideal Customer Profile (ICP),” even with a variety of alternatives. If you can’t answer this question, keep iterating.

4. What is the go-to-market strategy and business model viability?

While fintech is not always the easiest model to understand, when we hear, “it’s a complex business model,” this always raises a yellow flag. Successful go-to-market motions and business models have to be clear and digestible to your ICP, and your model must align you and your customer for joint success.

Often the most successful models align usage to increased pricing, joining the increased value an organization is receiving to increased pricing. Thoughtful minimums and tiers are critical here with definable attributes that drive prices — for example, a certain number of API calls.

If you’re building something in the fintech space, we’d love to speak with you. You can reach us at lars@unusual.vc and tyler@unusual.vc.