At Unusual we’ve built our entire firm around helping founders navigate the path from Idea to Product-Market Fit. Our Unusual Method charts the specific milestones a founder in today’s market needs to reach to be in a strong position to raise a Series A financing and build an iconic company. We counsel founders to raise money at every stage with a detailed plan in place to achieve a set of goals before the next fundraise. Unfortunately, there are times the market’s requirements for raising the next round can change midway through the journey and the burden falls to founders to find a way to adapt.

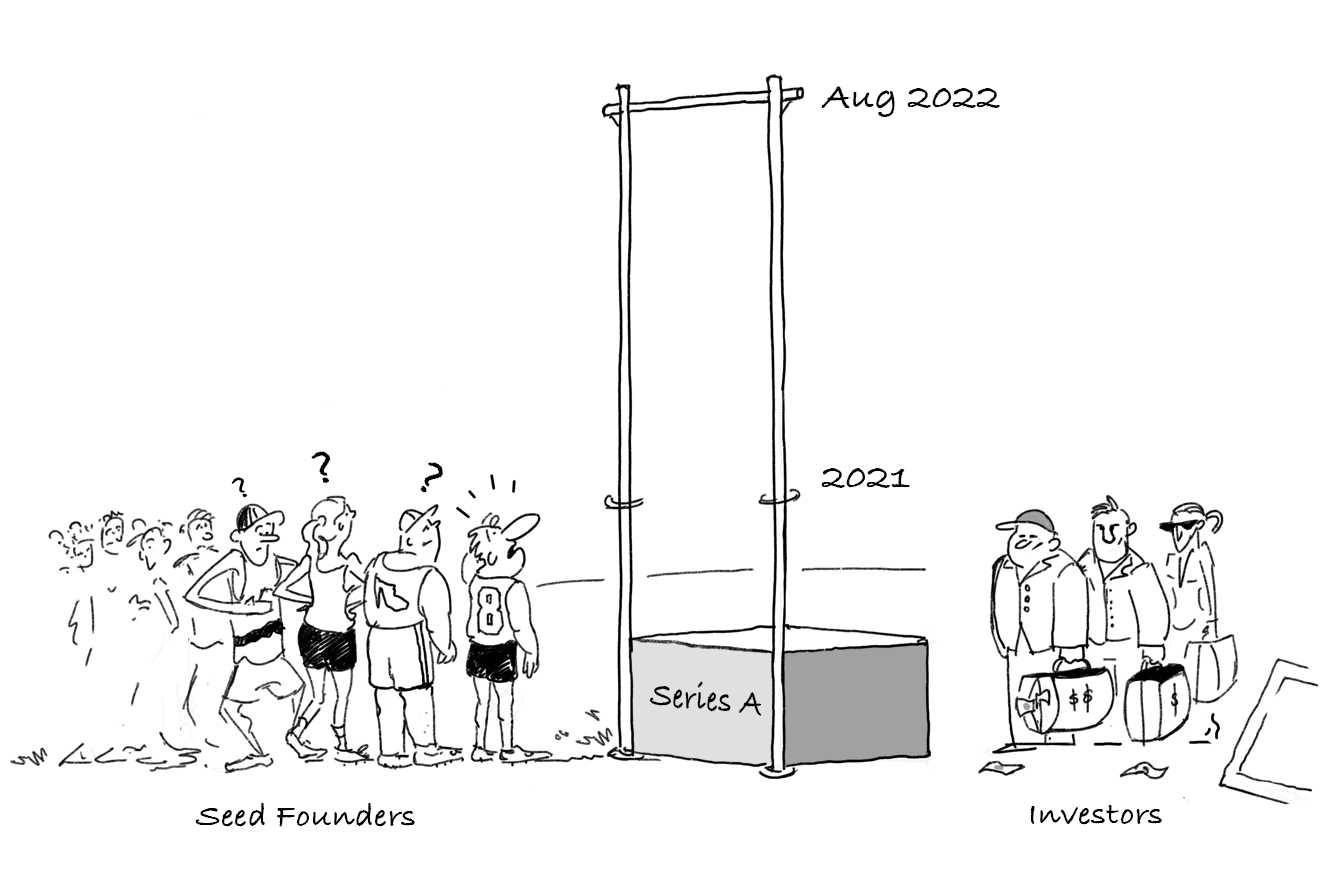

While one could certainly argue that it’s never fair to move the goalposts in the middle of the game, cursing the bad luck isn’t going to help! The good news is most founders are incredibly resilient and can often work closely with their Seed investors to understand where the market for the next round of funding is and steer the business to hit the necessary goals. As we enter the back half of 2022, there’s no doubt that the bar for raising a Series A has gone up significantly compared to 12 months ago. What’s most important now for founders is knowing where the new bar is.

For the past decade, the level of traction Series A investors said they wanted to see before seriously engaging in a financing discussion was “approaching $1M in ARR.” This is a commonly accepted industry watermark for signaling a company has achieved Product-Market Fit. The next phase of the company’s evolution is to scale the go-to-market machine — precisely the level of risk many investors prefer to take. Consistent with this way of thinking, we witnessed a wave of newly minted Associates, Principals and Partners at many venture firms scouring the startup universe, tasked with unearthing promising startups with this metric as the primary signal to look for. When they found it — or anything remotely close — they would put on the full-court sales press, sometimes overwhelming founders with proactive references, extensive investment memos, fancy dinners and aggressive financing terms so they could help their firms put that recently raised megafund to work.

In 2020 and 2021 things reached peak froth as what Seed stage founders experienced practically was a Series A investor market where FOMO, new entrants and a surplus of capital were the primary drivers. Seeded startups needed little to no revenue to attract new investors. The idea of missing the next Snowflake, Stripe, or Databricks was so strong investors simply “rounded up” when looking at the financials of Seed stage companies — meaning, they would consider any revenue (and often no revenue) as close enough to PMF to move aggressively and issue a term sheet.

Valuation multiples paid reached historical highs but that was true at every round, so Series A investors felt confident taking on the risk at these prices because frequently Series B investors were swooping in less than 12 months later and paying 4-5x higher prices, and Series C investors doing the same, and Series D investors doing the same, and… All of this made being aggressive at the Series A stage look very smart. But then public market multiples tumbled and the dominoes started to fall, fast.

In 2022, with the concrete effects of inflation, a lingering pandemic and many public tech stocks down more than 60% being felt, things have changed in the Series A market. Investors have gotten a lot more disciplined about only investing in startups that have achieved (or exceeded) $1M of ARR and demonstrated a repeatable sales process. Startups with $200k to $500k in ARR, that only a year ago would have had no trouble lining up meetings with VCs, are now frequently being told, “let’s touch base in a few quarters.” And for the companies that have reached $1M of ARR, it’s no longer a done deal. When investors do engage, significantly more time is being spent diligencing the customer set in order to understand the quality of the existing customers and the consistency of the use case that is at the heart of the decision to purchase. Investors are looking for repeatability because that translates to more efficient growth for the business in the next phase and therefore a less risky investment for them. Clear and demonstrated repeatability to the tune of $1M+ in ARR is a level of maturity few startups were funded to reach when they raised their Seed round. For many founders who are midway though their Seed journey, it feels like Lucy pulling the football away at the last minute!

Whereas in 2021 Seed stage startups were often closing Series A financings while still squarely in the “founder selling” phase of maturity, the new expectation from investors is that the company has progressed into the next phase. Any experienced founder will tell you it’s a massive jump to go from founder selling to the next level where the startup is demonstrating a hired group of initial Account Executives can be productive selling. But that’s where the new bar is in order to raise a Series A in 2022.

The reality now is that having a few paying customers is insufficient to put a Seed stage company in a strong position to raise a Series A. From 2018-2021, many Seed stage founders raised an amount of capital that was meant to provide the runway to hire an initial team, build 1.0 of the product, and have enough time to close a few paying customers. But in 2022, founders need to provide more existence proof they’ve achieved Product-Market Fit. That likely means others have been hired who are successfully selling the solution. Why? Consider the following math: most B2B companies have an Average Selling Price in the $20K to $40K range in the early years. That means in order to reach $1M of ARR, the startup must have somewhere between 25 and 50 customers. It’s likely that in order to reach that level of traction, the company is going to need a few more quarters of selling than the founder initially budgeted for and some additional resources to close business.

Here are a few thoughts for consideration as you plan for the new reality:

Fair or not — who said this was going to be easy! — the market for Series A has been reset in 2022. Investors have made a significant shift in their thinking and are requiring more proof of Product-Market Fit and the revenue to back it up. There’s a lot less “rounding up” going on as investors are suddenly disciplined about startups reaching $1M+ in ARR to seriously consider a Series A financing. The net result is that rather than Series A as the next step in the financing journey, many founders are looking at Seed extension rounds to reach the new, higher bar. The good news for founders is that high-quality Seed investors are built for just this kind of adjustment. At Unusual, we’ve been very active working with our existing founders and many new founders to adjust midstream, recalibrate on what it is going to take to successfully raise a Series A, and put a concrete plan into place along with new funding to reach the next peak. If you have any questions, feel free to reach out to learn@unusual.vc, we’d love to hear from you.

Onward!