When we launched the Field Guide, we knew we wanted to offer meaningful guidance around common startup challenges, and we knew we wanted to make it free to anyone starting a company.

We never expected the overwhelming response from founders who have requested specific topics, ranging from product-led growth to turnkey sales scripts.

Keeping a tight feedback loop with our audience has always been important and has allowed us to fill in the gaps and expand our library of startup knowledge over time.

One of the most common requests we’ve received is for expert advice about the earliest stage of the founder journey: taking the startup plunge.

There’s no shortage of advice out there on how to grow a company. But amid all the noise, we’ve found that very few sources dig deep into the nitty-gritty “how” of starting a company.

We talked with more than 30 early-stage founders who shared their stories of how they navigated the roller coaster of starting a company.

We also weaved in the investor perspective from Team Unusual. This guide features the collective wisdom that we believe will be helpful to early-stage founders just getting started.

Editor’s Note: We recognize that every founder’s journey is unique and that the path isn’t linear. As you read, keep in mind that the steps can occur in a different order depending on your own circumstances. Second, this is intended to be an overview of the very first phase of getting started and the journey ahead, not an exhaustive step-by-step manual. We hope the Field Guide can offer more in-depth insight on each step along the way!

Before you begin, ask yourself this critical question: “Why am I interested in starting a company?” Describe your motivations clearly and honestly. Are you excited by the thought of making a dent in the world, or is it something else?

Starting a company is a tremendous commitment where the odds are oftentimes stacked against you. Sarah Leary, Unusual Ventures partner and co-founder of Nextdoor, suggests having a “sit-down” conversation with yourself.

“If you aren’t really honest with yourself from the beginning and mentally prepared to go through the ups and downs of the startup journey, you’ll be in for a rude awakening. It’s an all-consuming journey that will test every bit of your fiber. Why do you want the stress of starting a company? You have to find motivation in the journey itself — not just the outcome you hope for. If you are honest with yourself, you’ll have a much better chance of surviving and even thriving.”

— Sarah Leary, Co-Founder of Nextdoor and Unusual Ventures Partner

Starting a company is a multi-year commitment and affects not only you but the people in your life.

Startup life might mean working longer hours and less time to spend with your kids or significant other. It might mean leaving behind a cushy job until you can fundraise for your idea. The bottom line: there will be a lot of uncertainty baked into your life as a founder.

Confirm with your family and anyone else who might be impacted that you have their full support and they understand what you’re getting into.

As Jyoti Bansal, co-founder of Unusual, AppDynamics, Harness, and Traceable says, “Starting a company is already a tough undertaking. Support from your personal network is what helps you get through the ups and downs.”

Keep in mind that your family might not understand the nature of the journey. Even with a father who ran his own business, Jyoti still faced skepticism.

When he told his parents he was starting a company, his father’s first question was, “What will the profit be?” Jyoti had to tell him there likely wouldn’t be a profit for multiple years.

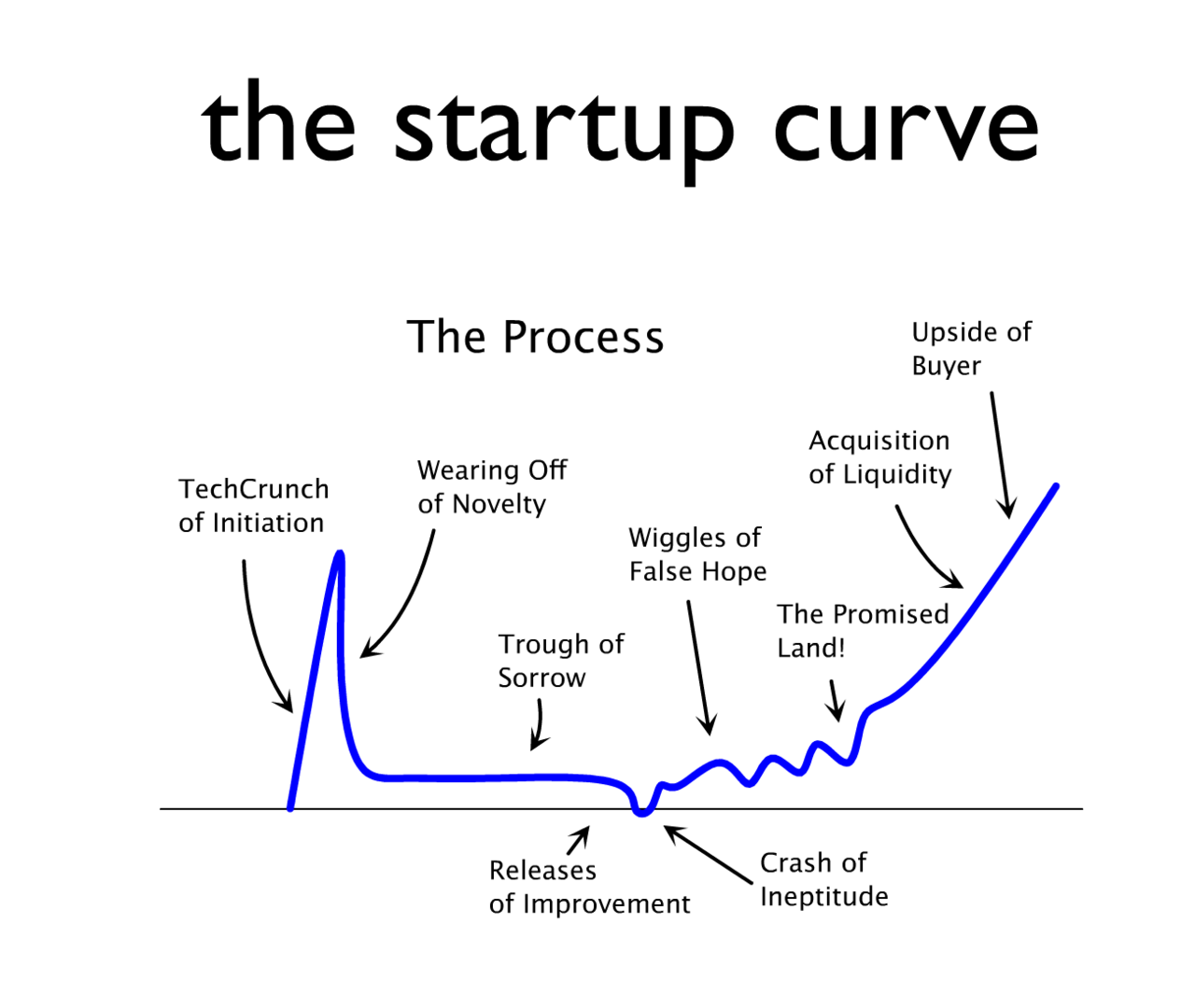

The more mentally prepared you are for the startup journey, the easier it will be when inevitable challenges arise. To all new founders and to the first 10–15 employees, Jyoti now shows what’s known as the “startup curve” to demonstrate the unpredictability of startup life.

“It might be a little cheesy, but it gives them an idea of what to expect. You have to be ready. The first valley you encounter will be so frustrating if you don’t anticipate it.”

Even with caution, it’s still impossible to go in with eyes completely wide open, and no founder will ever be 100% prepared for the roller coaster that is startup life.

In fact, that starry-eyed belief in the face of daunting odds is part of what makes taking the leap possible in the first place. As one founder we spoke to put it, “For me, the biggest risk was NOT starting a company versus any fears I had of failing.”

Our goal with this guide is to provide an honest take from experienced founders so you can do a real gut-check and proceed with an informed perspective. If you’re still reading and still interested in starting a company, great! Let’s talk about honing in on your insight.

How does one discover the next great startup idea? More often than not, lightning doesn’t strike overnight or come from brainstorming sessions.

When you ask successful entrepreneurs about how they arrived at their unique insight, many relate their own stories of a problem they faced on a regular basis — a gnawing pain that prompted them to build something that “scratched their own itch.”

Insights don’t just come to those looking to start a company. Insights are problems that you encounter in your own daily life and believe deep down can be solved in a better way.

The number-one consistent message we heard from founders is that there must be something wrong that you want to make right — so much that it’s nearly always on your mind.

To build a successful company, you have to find some shared pain that many people feel, and ideally, it starts with you.

Here’s Michael Krakaris discussing how he came up with the idea for Deliverr based on the pain points he and his co-founder, Harish Abbott, encountered in the fulfillment space.

Once founders identify the wrong they want to make right, most reach out within their network to see if others feel the pain too.

For the validation phase, you’ll want to cast a wide net. For example, Sarah Leary’s hit rate was about 30% with cold outreach to neighbors when she was validating the idea for Nextdoor.

The goal is to create a process for capturing initial reactions and noting any common themes that emerge from those early conversations.

As for the right number of customer interviews, founders agreed that a good rule of thumb was 30–50 customer interviews. While a dozen is not enough, the pain points in the customer feedback should start to converge by the time you reach 50.

For more guidance on enterprise customer validation, check out our 5-step framework. For guidance on consumer customer validation, check out our guide to finding product-market fit for consumer products.

Here’s Jyoti Bansal discussing his approach to customer discovery during the early days of building Harness — his second unicorn software startup.

You may want to start prototyping a solution. Thinking through a solution for yourself can help you gain greater conviction and clarity. As Jyoti says, he likes to dive right into building a prototype.

“I start building immediately as a way to dig into the problem. I have to convince myself that I can solve the problem in a new way. My advice to founders is to start coding. Don’t wait to start building. Prototype a potential solution. Any day with no code written is a wasted day.” — Jyoti Bansal, Unusual Ventures co-founder and serial entrepreneur

Even when he would be pitching customers all day, Jyoti would come back and write code to clarify his own conviction and keep the momentum on the solution.

Prototyping doesn’t mean you should build a full-featured solution. Instead, focus on building a prototype that is good enough to put in front of prospective customers and get feedback as quickly as you can.

For Nextdoor, Sarah used rough wireframes and mock-ups in her early user interviews to gauge early reactions and needs. The goal is to test your proposed solution in more realistic market conditions and continue learning.

You want to get answers to a few key questions about the product before you decide to build a company around it. Otherwise, you risk building in a vacuum and creating something that no one needs.

Here’s Sarah discussing Nextdoor’s prototyping process

At the same time you’re validating the market and your proposed solution, keep in mind that you’re also seeing if your customer “pitch” resonates and sparks excitement.

Reflecting on his experiences building three successful startups and one new venture capital firm, Jyoti recalls, “It’s been very different in each situation.

The number-one thing I learned from each experience is that you have to try to sell from the very beginning.” Joyti believes that if you can’t convince people your product is a good idea during the customer validation phase, it’s probably not an idea worth pursuing.

“You may not be able to convince more than 50% of the people you talk to, and that’s fine. If everyone thinks it’s a good idea, something is probably off as well. But if you can’t convince anyone, that’s a red flag. You’ll need to convince investors, early hires, and customers down the line so selling while you validate is critical.” — Jyoti Bansal

The best founders have real conviction in their idea because their insight comes from authentic experience, and it’s been battle-tested through ruthlessly objective market validation.

They understand at some level the challenges and the competition, and yet they have an unwavering belief in their unique edge and ability to win.

Note: A founder’s journey isn’t linear. There are some people who swap the order of finding an idea and finding a co-founder. Both paths are valid. The point is that at the end of this stage, you have an idea and team that fits together. That means you should only land on an idea that makes sense for the specific crew you’ve assembled to tackle together. By thoughtfully vetting for idea/team fit from the start, your chances of succeeding are that much higher.

Out of countless decisions you’ll make throughout the lifetime of your company, perhaps the most important decision you’ll make is choosing your co-founder(s).

It’s hard both emotionally and financially to undo this decision and change co-founders. There’s a human cost to doing this, and it can cause a lot of trauma inside an organization.

Remember that it takes time to find the right match — it’s not a decision you want to rush. Jyoti recommends mind-melding and playing to each other’s strengths.

“The ideal situation is someone you’ve worked with before that you really respect and admire. The most important thing is having alignment on the problem you’re solving and what the company is about. It’s about mutual respect, which goes beyond just trust. It’s about respecting each others’ strengths. A co-founder is not just a friend — they have to bring in skills that you admire and need. You want to make sure that ability to ‘mind meld’ is there and that you share the way of mentally thinking through things.”

— Jyoti Bansal

Picking a co-founder totally cold may also work, but there’s an obvious added risk. A good place to start is by tapping your personal and professional networks (for example, On Deck Fellowship, South Park Commons, Entrepreneur First, company alumni networks, school, mutual friends, etc.) and leaning on “super-connectors” (investors, previous colleagues, etc.) who might be able to introduce you to your future co-founder.

If you go this route, it’s critical to spend time working on a project together, designing and prototyping. Give yourself a trial period of at least a few months and check in regularly to see if the two of you are still interested in working together.

The road to building a successful company is often a lonely one, which makes having the right partner to lean on when the going gets tough even more important.

Sit down and have an open conversation with your co-founder(s) about expectations. Talk about your concerns and fears — whether they’re related to roles and responsibility, equity structure, board structure, desired outcomes, or anything else.

Engage in open dialogue, not just before taking the leap, but on a regular basis, so that you’re aligned.

The success of any startup often comes down to having the right team in place to execute on the idea from the very beginning. Co-founders should not only complement each other’s skills but also align around their vision for the company.

If you don’t find an ideal co-founder initially, you can start your business on your own. Jyoti didn’t have the energy and space to start a third company himself, so he waited 18 months before starting Traceable because he wanted the right co-founder.

He had not planned on starting a venture firm until possibly later in his career, but when the opportunity presented itself with John, someone he had known for over 10 years and worked very closely with in the early years of building AppDynamics, they decided to do it together.

Ultimately, you need to have bedrock-level conviction in yourself and your founding team. Do you truly have some unique experience or exposure that will help you win?

For instance, it could be your ability to assemble a great team or your prior execution record. In many ways, investors will hold you to that same standard, so it’s worth thinking through early.

One of the decisions you’ll have to make at the Pre-Seed Stage is deciding whether to raise outside capital. There are several reasons you might want to raise capital.

Having an investor involved can help mitigate some of the risk and add expertise to help you navigate the road ahead.

Typically, you raise a Pre-Seed round with the goal of hiring one to three people and using six to 12 months to figure out if this is an idea you want to commit to for the next seven-plus years. Some people skip this step or choose to bootstrap.

Skipping straight to a seed round can be appropriate when the insight and conviction are clearer, and they’re ready to raise a $3M+ round.

Start by asking yourself, “What do I need to do to make progress?” For most Pre-Seed startups, that means building a product, validating the idea in the market, and finding PMF. You need some notion of the milestones you want to achieve, separate from the fundraising element.

What does success for the next six to 12 months look like? Once you have that idea in your head, find a way to fund it.

Can you find ways to capitalize yourself through sweat equity or putting your own money in the company? If you are not in that position or if you want to have partners with you from the beginning, then you will need to find the right investors.

“If you want to be president, you don’t just wake up one day and decide to do it. Generally, most people build up a profile and a skill set over time in order to be prepared. Talk to other founders. Nurture investors, customers, and your potential team from day one. Set up a spreadsheet and run it like any other project you would tactically manage. Process and structure matters.” — Abhi Sharma, co-founder of Relyance

Try to build relationships with investors before you actually raise funding. Many investors are one introduction away and more than willing to get to know smart operators who might start a company someday.

Building relationships early gives you the chance to create a shortlist of the firms and investors you actually want in your future cap table.

When you do go out to raise money from prospective investors, Jyoti advises founders to time-box the process (approximately four weeks) and hit three things in every investor pitch:

Remember that venture capital investors have different criteria than individuals. Professional investors are looking for outsized returns and opportunities that can result in a company large enough to have an IPO. This is how the venture model works.

Every venture investor wants to make investments where, if all goes well, your idea becomes an iconic company that generates enough proceeds to cover all their other investments that didn’t work out and has plenty left over.

Investors want any proof points you can provide that the opportunity is de-risked. It could be customer conversations or market validation from experts, but investors want proof that you’ve done work to support your conviction that your idea could work.

The better your validation, the higher your valuation will be.

Investors often get pitched the same idea — by different people. It takes the right team to execute and bring an idea to life.

What’s special about you that sets you up to win over the competition? What’s your unique strength? Raising money successfully requires you to sell yourself and your skill set well.

For more guidance on the fundraising process, see our Unusual Guide to Raising a Seed or Series A: Pitch and Process and our Case Study on Raising a Seed.

Similar to selecting a co-founder, you don’t want to rush the decision of finding the right investment founder.

You want an investor who’s a good match for your idea and can bring relevant expertise and skills to the company you intend to build. Remember that in a best-case scenario, you’ll work with this individual for 10 or more years, and that it’s nearly impossible to fire your investor.

If you’re in the fortunate position to have multiple term sheets to choose from, we advise picking the right investor for the stage you’re at — one who will actually help you succeed.

As a startup founder, the odds are already stacked against you, and you want someone in your corner who will do the work to make sure you continue through to the next phase.

“My number-one piece of advice is to find an investor who believes in the problem you’re solving and you as an entrepreneur. You want someone sincerely interested in helping you grow as a founder. There’s plenty of capital out there. You don’t want the investor who will help you four years down the road. You need the investor who will help you now.”

— Jyoti Bansal

Above all, choose an investor you can trust. During the fundraising process, if you have conversations with folks who don’t feel quite right or trustworthy, don’t move forward.

Trust your gut and do your diligence. Ask for references from founders they’ve worked with before who can point to concrete examples of how that investor helped.